Big Update from April 2026: Form 15CA/15CB to be Replaced – Complete Guide to New Rules

The Government of India has introduced a significant update in foreign remittance compliance under the new Income-tax Act, 2025, effective from 1 April 2026. The existing Form 15CA and Form 15CB will be replaced by new Forms 145 and 146, bringing a revised reporting framework for payments made to non-residents. While the core objective of ensuring proper tax deduction at source (TDS) remains unchanged, taxpayers and professionals must adapt to the new formats, updated procedures, and compliance requirements under the new law. This guide explains everything you need to know about the transition, applicability, and key rules.

Form 15CA/15CB Amendments in AY 2026–27: Complete Analysis Under New Tax Law

The Government of India has introduced a significant update in foreign remittance compliance under the new Income-tax Act, 2025, effective from 1 April 2026. The existing Form 15CA and Form 15CB will be replaced by new Forms 145 and 146, bringing a revised reporting framework for payments made to non-residents. While the core objective of ensuring proper tax deduction at source (TDS) remains unchanged, taxpayers and professionals must adapt to the new formats, updated procedures, and compliance requirements under the new law. This guide explains everything you need to know about the transition, applicability, and key rules.

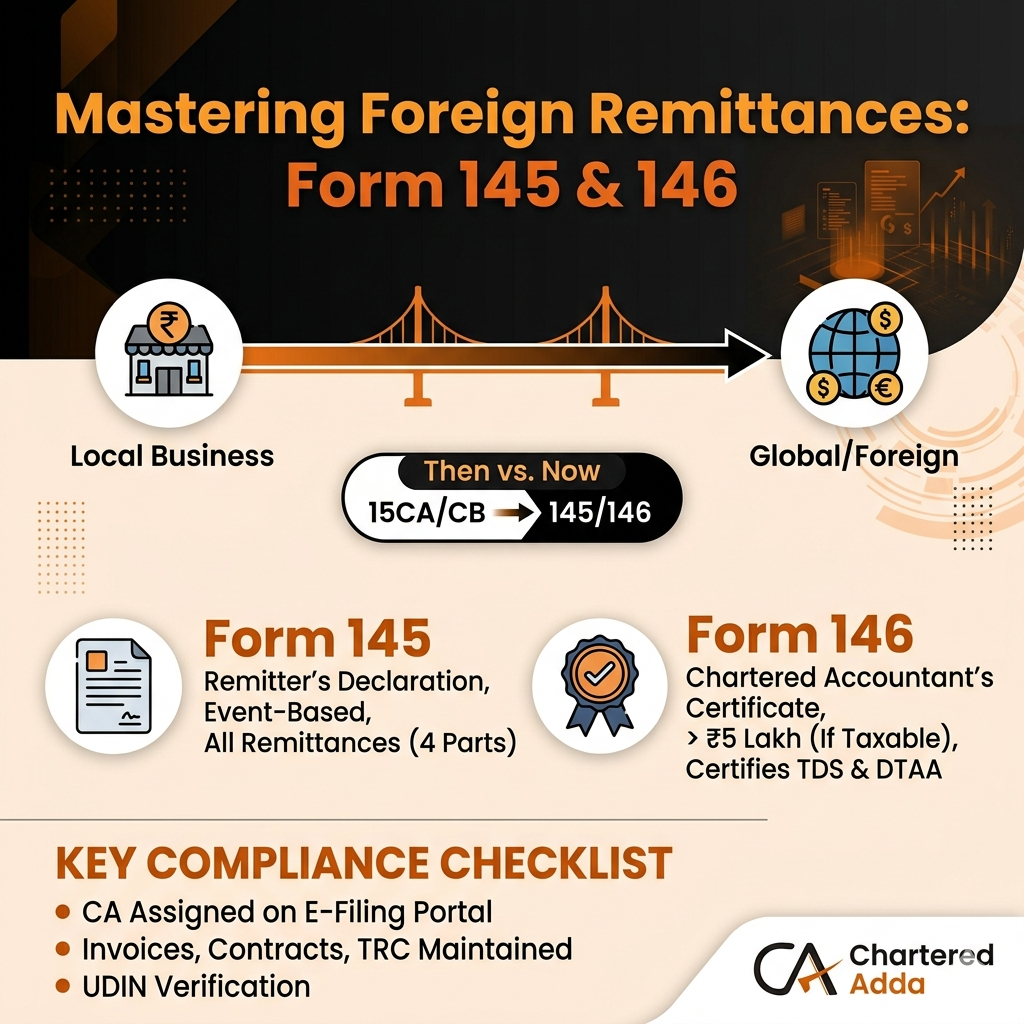

Transition from Form 15CA/15CB to Form 145/146 Under Income-tax Act, 2025

| Particular | Old System | New System (2026) |

|---|---|---|

| Forms | 15CA & 15CB | 145 & 146 |

| Applicable Law | Income Tax Act, 1961 | Income Tax Act, 2025 |

| Declaration Form | Form 15CA | Form 145 |

| CA Certificate | Form 15CB | Form 146 |

| Reporting Style | Basic details | Detailed & structured |

| Validation | Manual | System-based validation |

| Error Chances | Higher | Reduced |

| Processing | Slower | Faster & automated |

| Transparency | Limited | High |

| Effective Period | Up to 31 March 2026 | From 1 April 2026 |

Scope and Applicability of Form 15CA & 15CB Under Income-tax Rules

The scope and applicability of Form 15CA and Form 15CB arise in cases involving payments made to non-residents or foreign companies. These forms are part of the compliance framework to ensure that appropriate tax is deducted at source (TDS) on such remittances in accordance with the Income-tax Act. Form 15CA is a declaration submitted online by the remitter, providing details of the payment and its taxability, while Form 15CB is a certificate issued by a Chartered Accountant certifying the nature of the remittance, applicable tax rate, and compliance with tax provisions.

The requirement to file these forms depends on factors such as the nature of the payment, its taxability in India, and the amount involved. Generally, Form 15CB is required when the remittance exceeds the prescribed threshold and is taxable, whereas certain transactions and specified payments may be exempt from these requirements. Understanding their applicability is essential for individuals and businesses to ensure proper compliance, avoid penalties, and facilitate smooth foreign remittances.

Updated Rule 37BB Exemption List for 2026: Key Changes Explained

- Specifies cases where Form 15CA & 15CB are NOT required

- Applies to non-taxable or specified exempt remittances

- Helps reduce unnecessary compliance burden

- Expanded exemption list for practical transactions

- Better clarity on non-taxable remittances

- Alignment with new Income-tax Act, 2025 framework

- Certain import payments

- Overseas travel expenses

- Education-related remittances

- Other specified payments under Rule 37BB list

- Exemption applies only if conditions are satisfied

- Incorrect classification may lead to penalties

- Always verify if payment is truly non-taxable

- Faster bank processing of remittances

- Reduced documentation and compliance effort

Digital Shift in Remittance Reporting from April 2026

The digital shift in remittance reporting from April 2026 marks a significant step toward modernizing India’s tax compliance system under the Income-tax Act, 2025. With the introduction of new Forms 145 and 146 replacing the existing Form 15CA and Form 15CB, the reporting process is becoming more streamlined, data-driven, and fully integrated with online tax systems. This transition emphasizes end-to-end digital filing, real-time validation, and improved transparency in cross-border transactions.

The updated framework is designed to reduce manual intervention, minimize errors, and enhance efficiency for both taxpayers and professionals. It also enables better tracking of foreign remittances by tax authorities, ensuring accurate reporting and compliance with TDS provisions. As a result, businesses and individuals involved in international payments must adapt to these digital processes to ensure smooth and timely remittances.

Key Differences Between Old Forms (15CA/15CB) vs New Forms (145/146)

| Particular | Old Forms (15CA / 15CB) | New Forms (145 / 146) – 2026 |

|---|---|---|

| Applicable Law | Income Tax Act, 1961 | Income Tax Act, 2025 |

| Form Type | 15CA (Declaration) / 15CB (CA Certificate) | 145 (Declaration) / 146 (CA Certificate) |

| Effective Period | Up to 31 March 2026 | From 1 April 2026 |

| Reporting Format | Basic & semi-structured | Detailed & fully structured |

| Data Entry | Manual-heavy | System-driven & guided |

| Validation | Limited checks | Real-time system validation |

| Error Chances | Higher | Significantly reduced |

| Technology Use | Basic portal filing | Advanced digital integration |

| Transparency | Moderate | High transparency |

| Processing Time | Slower | Faster & automated |

| Tracking | Limited tracking | Better transaction tracking |

| Compliance Level | Standard | More strict & accurate |